Investing for your children's future: savings or funds?

Zoé Guelenne·22 December 2024·6 min read

Comparative analysis to make the right wealth decision.

The savings account: the false friend of your children's savings?

According to a study by the family allowance fund Camille, more than 70% of Belgian families who save for their children choose the savings account. Conversely, only 10% of families dare to explore other options such as investment funds, for fear of risk.

It is legitimate to wonder whether the savings account is really the most relevant solution for building a child's capital. Between 2003 and 2023, its average annual return was only 1.11% in Belgium, whereas inflation averaged 2%. In other words, savings were not enough to offset the rise in prices over this period, leading to a loss of purchasing power – a paradox for a product intended to grow your children's capital.

Financial education in Belgium: a gap that costs savers dearly

This reluctance to take risks is largely explained by a lack of financial education. According to a Febelfin study conducted in March 2024 among more than 2,000 Belgians, the lack of knowledge comes second among the reasons that hold back investment, just behind the lack of means.

There is nothing surprising about this: economics is often optional, or even absent, when it comes to portfolio management in Belgian secondary education, and few university courses offer in-depth training on financial concepts. This educational gap leads to a lack of awareness of the opportunities of the financial markets and to an exaggerated fear of loss for a large part of the Belgian population, whereas doing nothing in itself carries a very real risk: that of letting inflation erode the value of one's savings.

Lessons from Aunt Agathe: investing to beat inflation

After putting the savings account on public trial, let us see, with a concrete example, what an investment in an index fund could yield by comparison. Often shunned when it comes to saving for one's children, these funds nonetheless conceal a potential that is just waiting to be revealed through wise and considered management.

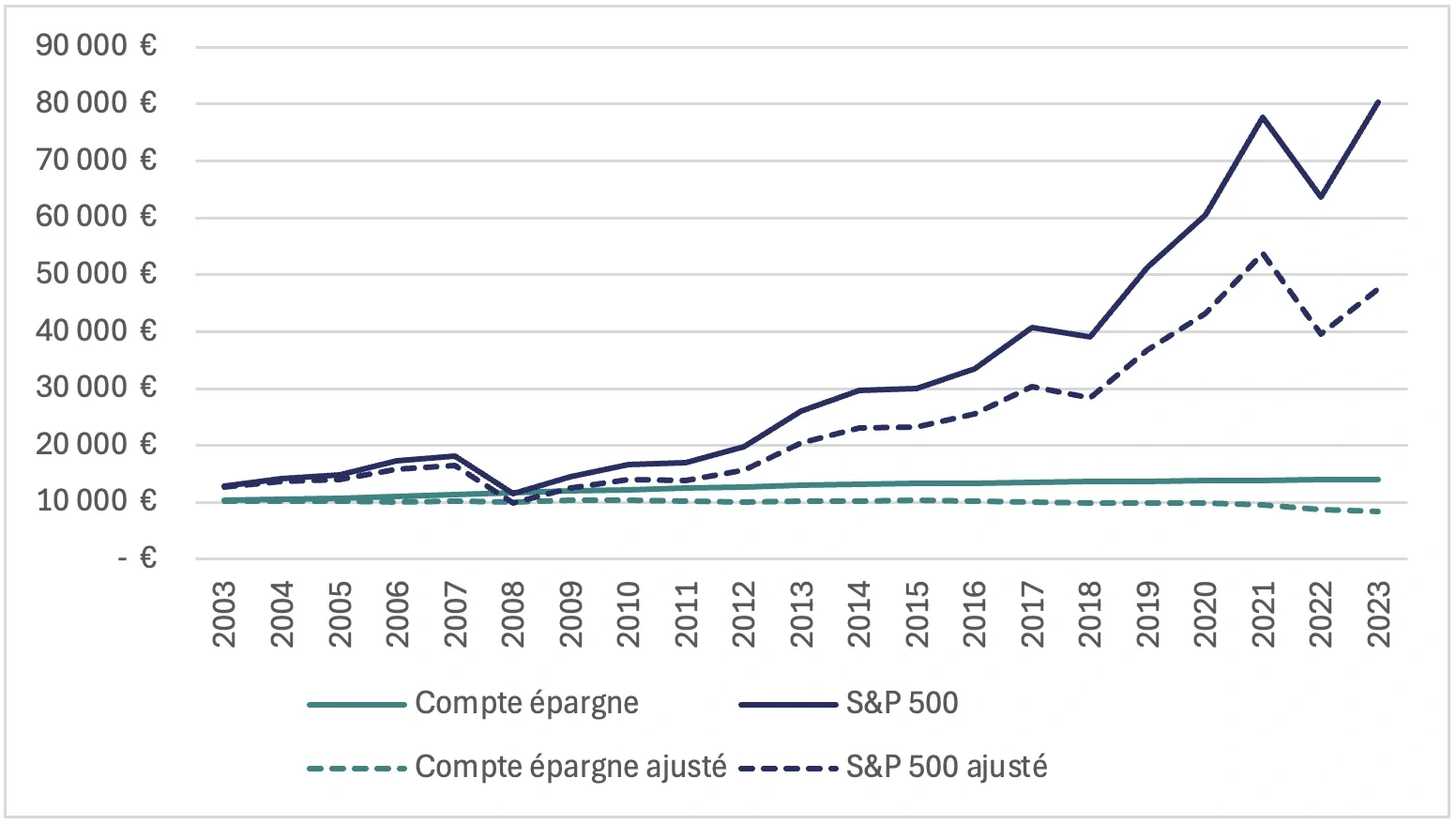

Let us rejoin our dear Aunt Agathe and her brother Uncle Séraphin. In 2003, these two happy grandparents decided to make a spontaneous donation of 10,000€ to their grandchildren. Aunt Agathe, comfortable with the financial markets, decided to place it in a fund replicating the S&P 500 index. For his part, Uncle Séraphin, more cautious, opted for safety by placing the same sum in a savings account1.

The years passed and, in 2023, the results speak for themselves: Aunt Agathe's grandson pockets more than 80,000€ while Uncle Séraphin's granddaughter recovers… 14,000€. The picture is far bleaker when inflation comes into play. Indeed, the chart shows that inflation nibbled away at the capital in the savings account, leaving Uncle Séraphin's granddaughter with purchasing power lower than what had been invested 20 years earlier.

Chart 1 – Change in the value of a 10,000€ investment in an S&P 500 index fund and in a savings account from 2003 to 2023, compared with their inflation-adjusted value

Long term and diversification: the keys to success

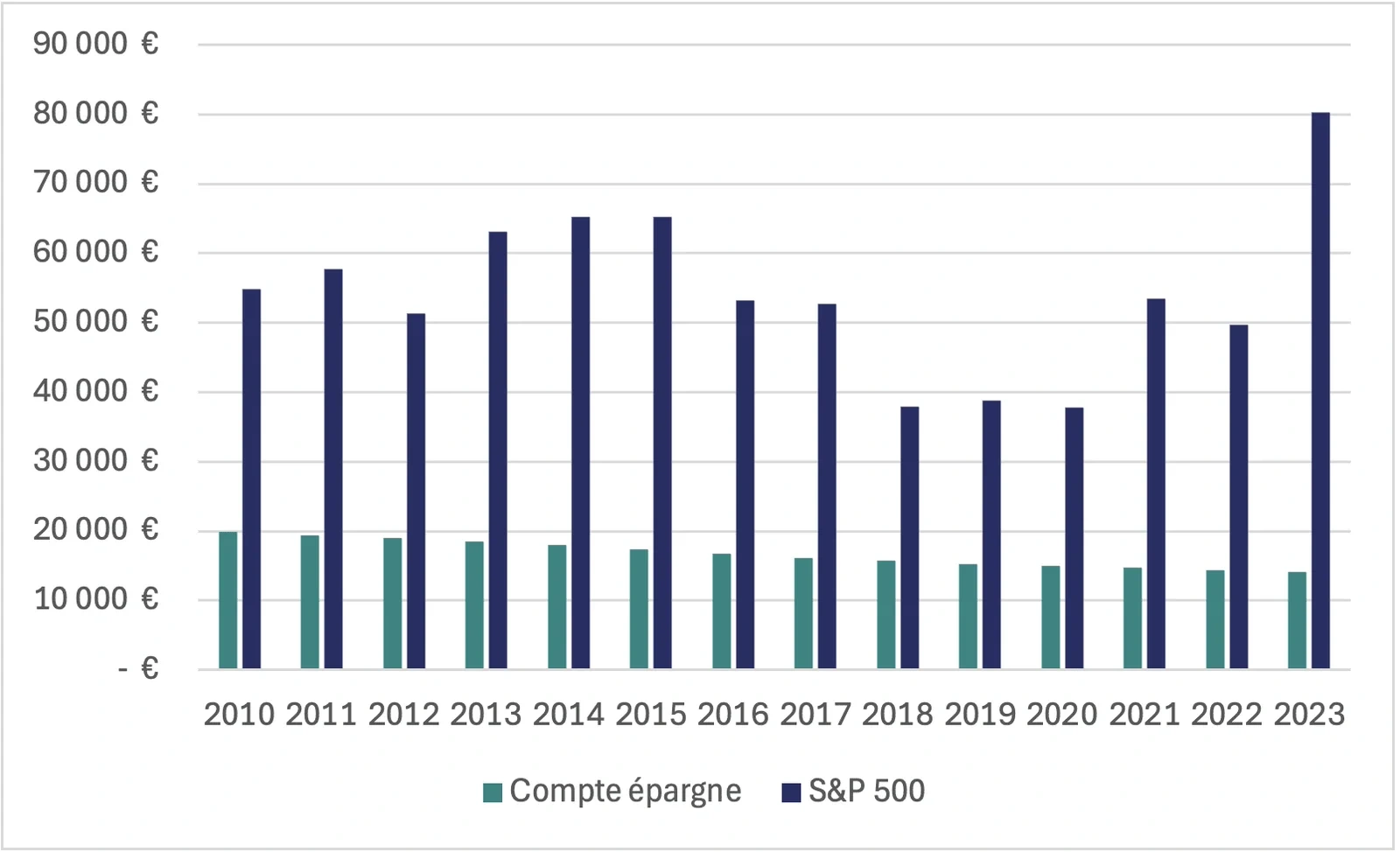

Aunt Agathe was not simply lucky. Her success rests on a proven strategy: investing over the long term and diversifying her investments – both in terms of assets and over time. This temporal diversification, although omitted in our example for reasons of graphical clarity, is essential to smooth out the risks linked to market fluctuations. The Chart 2 is an illustration of this: the value obtained after 20 years thanks to a single investment of 10,000€ in an index fund replicating the S&P 500 systematically exceeds the performance of the savings account. However, these results vary considerably depending on the starting year.

This ability of stock market investments to outperform over the long term is also reflected in the overall numbers: between 2003 and 2023, the diversified fund in which Aunt Agathe invested generated an average annual return close to 10%. By comparison, the average annual return of 1.64% offered by the savings account chosen by Uncle Séraphin pales in comparison.

Long-term risk: a question of perspective

Of course, market volatility can be worrying in the short term. However, when it comes to a long-term investment, such as one made for a child, these fluctuations are generally absorbed over time. For example, an investment of 10,000€ in a fund replicating the S&P 500 just before the 2008 crisis would have recovered its initial value in around four years, despite the collapse of the markets3.

That said, knowing your risk profile remains essential. Depending on this profile, it may be relevant to diversify your investments with low-risk assets, even over the long term. However, the longer the horizon, the more potential losses are mitigated and the more the potential for return increases. Consequently, a long-term investor is generally able to accept a higher level of risk than a short-term investor.

Chart 2 – Change in the value of 10,000 € after 20 years: comparison between a savings account and the S&P 500 (1990-2003)

Conclusion: do not let fear and inflation eat away at your returns

Investing regularly, whether monthly or quarterly, in a well-diversified equity portfolio can make it possible to tame market volatility while generating returns clearly higher than those of savings accounts.

Admittedly, the financial markets carry risks, but failing to take advantage of them and letting your savings erode under the effect of inflation is a risk in itself.

Do not let a lack of financial knowledge limit your returns and those of your children. Train yourself, gain confidence and optimise your investments according to your objectives and your risk profile. With the Portfolio Management training offered by Sagora, you are one step away from getting started successfully.

Would you like to navigate the turbulent waters of the financial markets more serenely? Do not hesitate to visit our website to discover our Portfolio Management training programme: https://sagora.eu/fr/formation/gestion-de-portefeuille/!

Campart, S. (2018). Et si on osait investir ? EMS Editions.

Damodaran, A. (2024). Historical Returns on Stocks, Bonds and Bills: 1928-2023. https://pages.stern.nyu.edu/~adamodar/NewHomePage/datafile/histretSP.html

République Française, Service Public. (2023). Livret A. https://www.service-public.fr/particuliers/vosdroits/F2365

(1) The annual returns of the Livret A (France) are used for the ease of access to historical data. Bear in mind, however, that the average annual return of Belgian savings accounts is even lower than that of the Livret A (1.11% versus 1.64% on average).

(2) This article is based on the performance of the American market, in particular that of the S&P 500. It is important to note that these results should not be extrapolated to all investment funds, especially European funds, which have not necessarily had comparable performance. By way of illustration, the Euro Stoxx 50 index took more than 16 years to recover its pre-2008-crisis level.

(3) Be careful, past performance does not guarantee future performance.