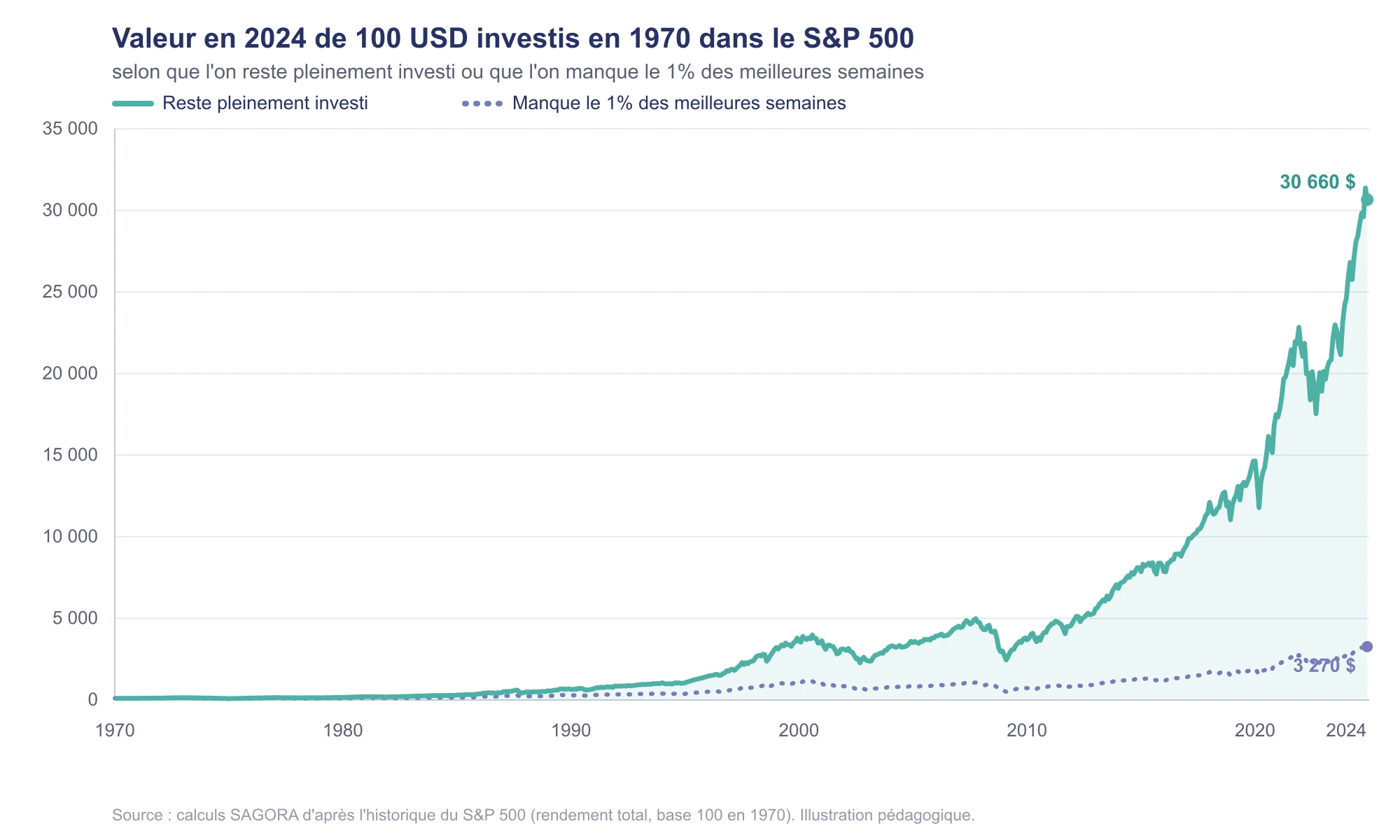

Don't panic: why patience is your best ally in turbulent times

In 2020, the S&P 500 fell by almost 35% before rebounding just as fast. In turbulent times, the temptation to sell is costly: the real risk is not the decline, it is missing the few days that make performance.

Related articles

At the same cost, AI transforms your financial analysis. The skill of judging it makes the difference.

The rare skill is no longer producing the analysis: it is knowing how far to trust it. AI only adds value when a human judges it. On the same budget, it then frees up time for what matters most: acting on the levers that create value. Getting trained and well advised is no longer an extra; it is what separates those who endure AI from those who extract real value from it.

Ziegler bankruptcy: three signals every leader must read

Behind Ziegler's bankruptcy, its 2024 accounts already revealed three signs of strain. A concrete framework for any leader who wants to see it coming: the structure of the balance sheet and the net cash position, EBITDA and the map of cash flows.

Does a monkey invest better than you (or than Aunt Agatha)?

According to Burton Malkiel, even experts cannot beat the market consistently, because performance is largely unpredictable and comparable to chance.