Robert Arnott's experiment

The most famous experiment for testing B. Malkiel's claim was conducted by Robert Arnott and his team. They simulated the choices of a monkey by randomly selecting 100 portfolios of 30 stocks from among the 1,000 largest market capitalisations, with each stock having the same weight in the index. This process was repeated every year from 1964 to 2012. And sure enough, it happened! Beyond Burton Malkiel's predictions, the monkeys beat the market 96 times out of 100.

The success of the chimpanzees: between chance and expertise

Should Aunt Agatha then rush to the chimpanzee enclosure to entrust them with her entire inheritance? Not exactly. It is all a question of weighting. In traditional index funds such as the S&P 500, the weight of each company depends on its market capitalisation. Conversely, the monkeys' index weights each company equally, giving smaller capitalisations more weight by default. These small companies have appealing growth potential and can offer substantial returns, offsetting the losses on other stocks. In fact, if we applied equal weighting to a traditional index, it would outperform the monkeys' experimental index funds.

However, as Nicholas Nassim Taleb, the famous writer and statistician, so aptly put it, if you put an infinite number of monkeys in front of typewriters, one of them will eventually type out an exact version of the Iliad. But would you bet all your savings on the idea that this same monkey will then write the Odyssey? For Aunt Agatha, that is out of the question!

The extraordinary performance of a few of the randomly chosen stocks does not guarantee that every choice will be a winner. Small capitalisations can pay off handsomely, but they also carry greater volatility. Original though she is, Aunt Agatha is reluctant to invest her parents' hard-earned money in this kind of random diversified strategy. The idea of beating the market by letting a monkey pick the stocks was above all a humorous way of illustrating that a random diversified investment strategy can perform just as well as a strategy with identical risk devised by experts.

The efficient market hypothesis

Nonetheless, this experiment illustrates an important point: the efficient market hypothesis in its semi-strong form. According to this hypothesis, market participants behave entirely rationally, and prices should reflect all publicly available information. So, if everyone holds the same information about a company and if everyone is rational, then everyone should assign the same price to that company's shares. The opposite would mean that some participants hold inside information.

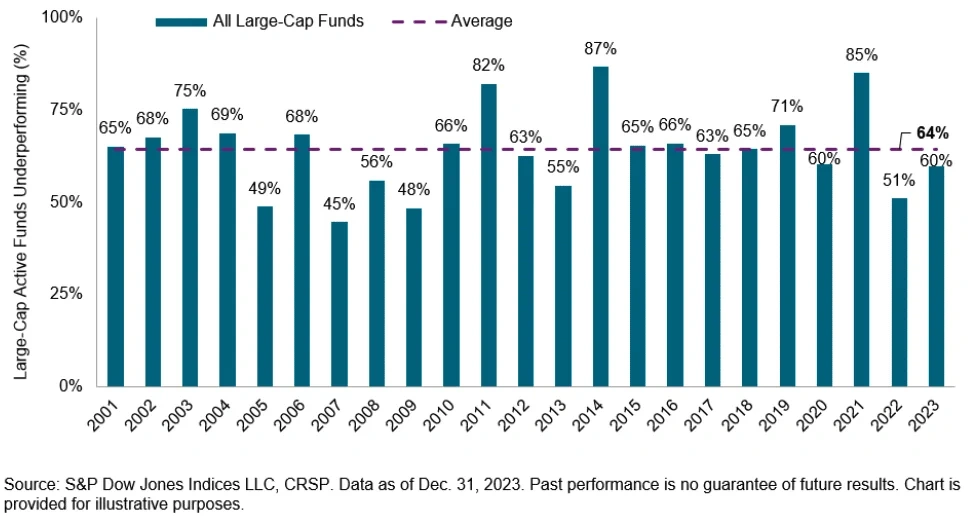

If this hypothesis is true, on average it would be difficult for fund managers to consistently outperform the market or to do better than a random portfolio (such as the monkeys'). This is illustrated, moreover, in Figure 1, where we can see that the majority of active large-cap managers underperformed the S&P 500 for the 14th year running.

Figure 1 - Most actively managed US large-cap equity funds underperformed the S&P 500 in 20 years out of 23.

Reducing fees to maximise returns

To conclude, Burton Malkiel does not compare experts to monkeys simply to provoke, but to illustrate that the stock market often follows the principles of efficient markets. Robert Arnott's experiment shows that random choices can sometimes outperform those of experts. Consequently, minimising management fees (which are higher in active management) by adopting passive management and investing in diversified index funds can be a sensible strategy for Aunt Agatha and many other investors.

That said, nothing stops you from setting aside a small part of your money, which you are willing to risk, for active management. After all, markets are not always perfectly rational. Your adviser can offer you a range of varied products, such as investments in private equity, in real estate, or in commodities. They can also offer you comprehensive financial services, such as tax and wealth planning, thereby optimising the management of your assets according to your life cycle. Although Robert Arnott's experiment calls active management into question, it takes nothing away from the added value of these personalised services.

Would you like to navigate the choppy waters of the financial markets more calmly? Do feel free to visit our website to discover our training programme in portfolio management!

#FinancialTraining #PortfolioManagement #PersonalFinance #Diversification #KnokkeSummerSchool

Sources

Ernst J. Fahling, Mario Ghiani, Diethard Simmert. (2020). Small versus Large Caps: Empirical Performance Analyses of Stock Market Indices in Germany, EU & US since Global Financial Crisis. https://www.researchgate.net/publication/347402716SmallversusLargeCaps-EmpiricalPerformanceAnalysesofStockMarketIndicesinGermanyEUUSsinceGlobalFinancialCrisis

Louapre David. (2013). Un singe ferait-il mieux que votre conseiller financier ? Sciences étonnantes. https://scienceetonnante.com/2013/11/04/un-singe-ferait-il-mieux-que-votre-conseiller-financier/

Robert D. Arnott, Jason Hsu, Vitali Kalesnik et Phil Tindall. (2013). The Surprising Alpha From Malkiel's Monkey and Upside-Down Strategies. https://thereformedbroker.com/wp-content/uploads/2014/11/jpmsummer2013rallc.pdf

Schmit, M. (2023). Banking and Asset Management. EU Fund Industry [Slides].

(n.a.). (2022). The monkeys that beat the market. Market Sentiment https://www.marketsentiment.co/p/the-monkeys-that-beat-the-market