Portfolio management and market volatility

Investment results fluctuate: they make you neither a genius nor an incompetent.

Understanding market volatility

It is often difficult to understand the evolution of the value of our investments. Sometimes they rise, sometimes they fall. Never seeming to make up their mind about the trend to follow, their evolution leaves us with a sawtooth chart that says little. Yet behind this child's scribble lies a veritable ballet of assets, whose mistress of ceremonies is none other than market volatility.

Indeed, the financial markets are very volatile. If one ventured to examine the historical returns of the famous S&P 500 stock market index from 1900 to 2023, and to rank each year according to its percentage return, one would find that in 95% of cases, the return lies between -30% and +50%. In other words, by investing 100,000 euros, you could earn between -30,000 and 50,000 euros per year! I grant you, this range is so wide that it would be almost like saying that the answer to the question "How are you?" lies somewhere between euphoria and affliction. And, even if you were rich enough or bold enough to accept the risk of losing 30% of your investment, do not forget that in 5% of cases, that is once every 20 years on average, the market can fall below -30% (or, similarly, rise above 50%). This happened in 2008, when the unfortunate ones who had decided to invest were faced with a tumble of -37%.

Yet such is the harsh reality of the markets. Returns can vary considerably from one year to the next, and even good diversification at the level of the assets in our portfolio does not constitute sufficient protection, much to the detriment of investors' comfort.

But is that all, then? If even a well-diversified portfolio is not enough, should one take back all one's marbles and let oneself be overwhelmed by the fear that the lightning of the markets will one day strike us? Fortunately, no, because we have another ally to help us in managing our portfolio: time diversification.

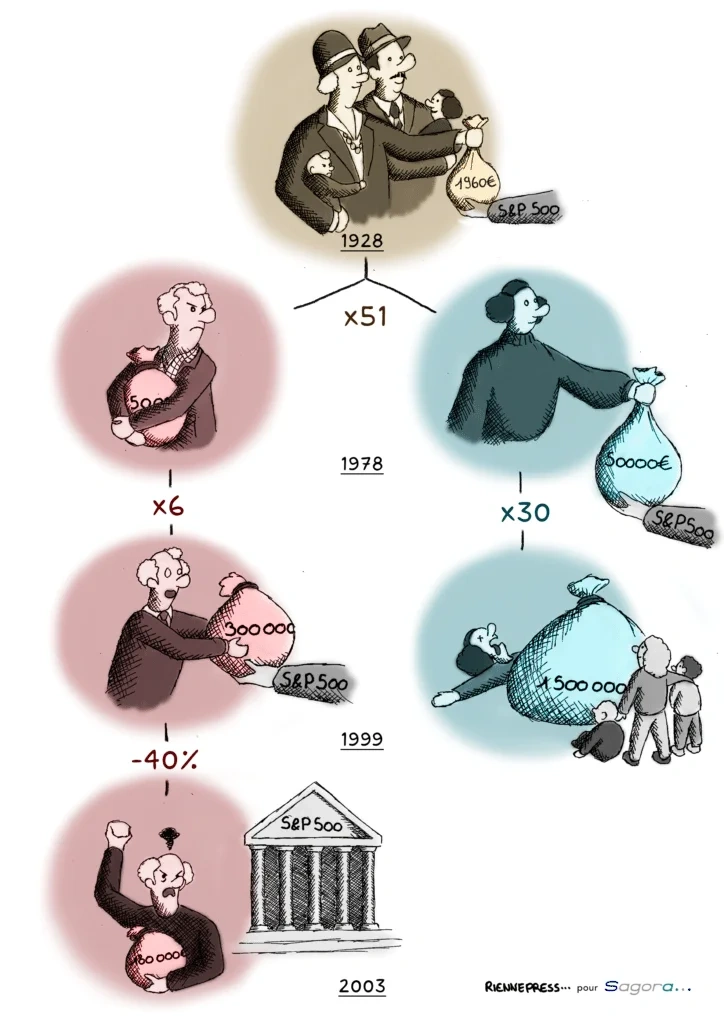

Investing in the stock market with Aunt Agathe

To properly understand what this is about, let us return to family stories and take the example of Aunt Agathe's. Let us take a closer look at her family's portfolio management...

Aunt Agathe's savvy grandparents

Aunt Agathe was lucky in life. Indeed, her grandparents, keen to leave an inheritance to their descendants and possessing certain financial notions, decided to place 1,960 euros in a highly diversified asset portfolio equivalent to the S&P 500 in 1928. On their death, 50 years later, this money was withdrawn to be bequeathed to their two children: Marguerite and her brother, whom we shall call Léon. Time having done its work, the two found themselves with a sum of around 100,000 euros, a 51-fold multiplication of the parents' initial investment!

Marguerite, the mother of cunning Aunt Agathe, and timid Léon

Marguerite, Aunt Agathe's mother, was not born yesterday, and therefore hastened to follow her parents' example by directly reinvesting her share in 1978, that is 50,000 euros, in the same stock market index. For his part, a bit of a stay-at-home and not trusting "his thieving bankers", her brother, Léon, placed them in a savings account.

Under the weight of regrets: the contrasting fortunes of Marguerite and Léon

Time passed and, in 1999, Aunt Agathe's mother kicked the bucket, and, having failed to show herself generous during her lifetime, she left an investment multiplied by a factor of 30, that is an amount of 1,500,000, to her children: Aunt Agathe and Uncle Séraphin, whose adventures we shall have the joy of following over the coming articles. Sensing his turn coming, and jealous of his sister's portfolio management success, Léon finally decided to enter the market at the start of the following year, with capital enriched by his savings of 300,000 euros. However, a victim of the bursting of the internet bubble, he quickly became disillusioned and hastily withdrew his money in 2003, after losing almost 40% of his initial investment. Humiliated by this mediocre performance, and rebuffed by those close to him who saw him as a finance novice, his hatred of bankers had never been so great.

Mastering one's financial investments with Agathe and Séraphin's family

Several lessons can be drawn from this story. First of all, the example of Aunt Agathe and Uncle Séraphin's grandparents and parents demonstrates the importance of adopting a long-term perspective when investing. Indeed, by placing their money very early, over several decades, they saw their initial stake multiply considerably, thus offering a substantial inheritance to their descendants.

Next, Léon's story demonstrates the importance of the moment of entry into the market. Indeed, by delaying his investment until the start of the year 2000, he missed a period of significant growth and was faced with a market downturn during the bursting of the internet bubble. Finally, Léon's failure shows us just how important time diversification is for optimal management of an investment portfolio. By investing regularly over the long term rather than betting everything on a whim, buoyed by his sister's success, he could have avoided the significant losses suffered following an extreme event.

Conclusion for serene and profitable portfolio management

To illustrate our point, we could continue this story with all of Aunt Agathe and Uncle Séraphin's descendants. For, on the financial markets, the unlucky ones, victims of extreme events and abrupt changes of course, are not in short supply.

Your success on the financial markets therefore depends on several factors that are sometimes beyond your control. This should not, however, intimidate you with regard to your investments. Indeed, over the long term (10 to 20 years), the markets bring an average annual return of around 10%, that is a doubling of one's capital on average every 8 years. It is nevertheless advisable to remain vigilant in the face of the very high volatility inherent in the financial markets. Consequently, the importance of your responsibility then lies in an appropriate diversification of your investments, both in terms of assets and of timing, and in the application of the concepts addressed throughout the article in order to take advantage of market volatility.

Key points to remember about portfolio management

-> The financial markets are very volatile.

Even well-diversified portfolios are very risky.

-> The timing of your entry into the market can have a significant impact on your investments, both upward and downward, hence the importance of spreading one's investments over time.

-> It is possible to reduce volatility by diversifying not only assets but also over time.

-> A long-term vision for your investments offers more opportunities to practise time diversification.

-> Risk is not, however, something to flee from and can be a source of substantial returns, taking into account the concepts discussed in this article.

-> In the long term, well-diversified investments such as the S&P 500 display an average annual return of 10%, although it is essential to remain vigilant about their significant volatility, which is mastered over the long term via asset and time diversification.

If you would like to navigate the choppy waters of the financial markets more serenely, do not hesitate to visit our website to discover our training programme in portfolio management!

References:

- Damodaran, A. (2024). Historical Returns on Stocks, Bonds and Bills: 1928-2023. https://pages.stern.nyu.edu/~adamodar/NewHomePage/datafile/histretSP.html

- Schmit, M. (2023). Banking and Asset Management. Understanding Banking Performance [Slides]. https://uv.ulb.ac.be/pluginfile.php/3821056/modresource/content/1/2022Handout2INGDirectFinancialrisks.pdf

Related articles

The stock market crash of 5 August 2024: a cold autopsy

A spectacular market crash, fuelled by disappointing economic indicators, geopolitical tensions and worrying signals around players such as Apple Inc. and Warren Buffett, shook the whole of the global economy.

A formidable animal, yet too rarely feared: the Black Swan

“Black swans”, popularised by Nassim Nicholas Taleb, are unpredictable events with major consequences, at once fascinating and feared by investors.

The man at the top of the Ponzi pyramid

The Bernard Madoff affair shows that, despite the rules, even financial systems can be manipulated by frauds such as the Ponzi pyramid.